Your 2023 Tax Fact Sheet and Calendar

Bookmark this guide to stay abreast of the tax-related dates and data that should be on your radar this year.

As we enter 2023, there aren’t many seismic changes scheduled, taxwise. Instead, most of the tax changes going into effect as the new year dawns amount to adjustments to income or contribution limits, reflective of the effects of inflation in various provisions within the tax code. Because inflation has been high recently, those inflation adjustments are also higher than usual.

Here are key tax-related dates and data points to have on your radar for the year ahead.

2023 Important Tax Facts for All Taxpayers

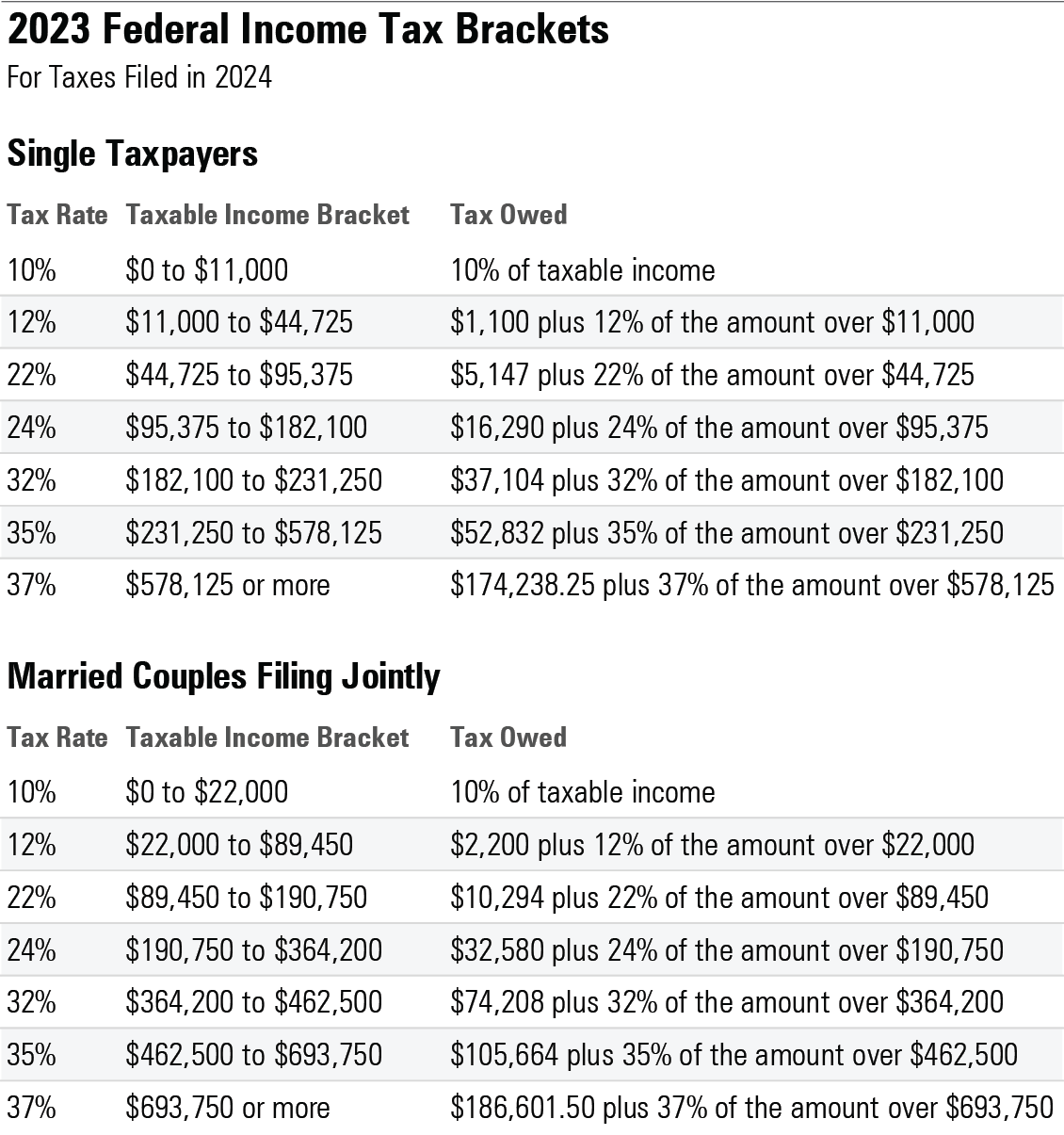

Income Tax Brackets: Seven tax brackets remain, but the specific parameters have changed, as follows:

2023 Federal Tax Brackets

Standard Deduction: Standard deduction amounts are increasing by a healthy amount in 2023, to $13,850 for single filers and $27,700 for married couples filing jointly. People who are over 65 or blind can claim an additional $1,500 per person for their standard deduction.

AMT-Exempt Amounts: The exemption amounts for the Alternative Minimum Tax are increasing slightly in 2023, to $81,300 for single filers and $126,500 for married couples filing jointly. The exemption amounts phase out for single filers with alternative minimum taxable incomes of more than $578,150, and $1,156,300 for married couples filing jointly.

Estate/Gift Tax Exemption: This amount is increasing in 2023, to $12.92 million per individual. The annual gift-tax exclusion is increasing to $17,000, up from $16,000. (Note that annual gifts in excess of this amount do not automatically trigger any sort of gift tax. Most people won’t owe estate or gift taxes in their lifetimes under current tax laws.)

2023 Important Tax Facts for Investors

Qualified Dividend and Long-Term Capital Gains Rates: Three rates are still in place for dividends and long-term capital gains—0%, 15%, and 20%—but they don’t map perfectly by tax bracket as they did in the past. Here are the parameters for each of the rates.

- 0%: Single taxpayers with incomes between $0 and $44,625; married couples filing jointly with incomes between $0 and $89,250.

- 15%: Single taxpayers with incomes between $44,625 and $492,300; married couples filing jointly with incomes between $89,250 and $553,850.

- 20%: Single taxpayers with incomes over $492,300; married couples filing jointly with incomes over $553,850.

Medicare Surtax: As in years past, an additional 3.8% Medicare surtax will apply to the lesser of net investment income or the excess of modified adjusted gross income over $200,000 for single taxpayers and $250,000 for married couples filing jointly.

IRA Contribution Limits (Roth or Traditional): $6,500 under age 50/$7,500 age 50 and over.

Income Limits for Deductible IRA Contribution, single filers covered by a retirement plan at work: Modified adjusted gross income under $73,000—fully deductible contribution; between $73,000 and $83,000—partially deductible contribution; more than $83,000—contribution not deductible.

Income Limits for Deductible IRA Contribution, single filers who are not covered by a retirement plan at work or married couples if neither spouse is covered by a retirement plan at work: None.

Income Limits for Deductible IRA Contribution, married couples filing jointly, if covered by a retirement plan at work: Modified adjusted gross income under $116,000—fully deductible contribution; between $116,000 and $136,000—partially deductible contribution; more than $136,000—contribution not deductible.

Income Limits for Deductible IRA Contributions, married couples filing jointly, if not covered by a retirement plan at work but spouse is: Modified adjusted gross income under $218,000—fully deductible contribution; between $218,000 and $228,000—partially deductible contribution; more than $228,000—contribution not deductible.

Income Limits for Nondeductible IRA Contributions: None.

Income Limits for IRA Conversions: None.

Income Limits for Roth IRA Contribution, single filers: Modified adjusted gross income under $138,000—full Roth contribution; between $138,000 and $153,000—partial Roth contribution; more than $153,000—no Roth contribution.

Income Limits for Roth IRA Contribution, married couples filing jointly: Modified adjusted gross income under $218,000—full Roth contribution; between $218,000 and $228,000—partial Roth contribution; more than $228,000—no Roth contribution.

Contribution Limits for 401(k), 403(b), 457 plan, or Self-Employed 401(k) (Roth or Traditional): $22,500 under age 50; $30,000 for age 50 and older.

Total 401(k) Contribution Limits, including employer (pretax, Roth, aftertax) and employee contributions and forfeitures: $66,000 if under age 50; $73,500 if 50-plus.

Income Limits for 401(k), 403(b), 457 Plan: None, though annual compensation limits can come into play in certain situations.

SEP IRA Contribution Limit: The lesser of 25% of compensation or $66,000.

Saver’s Tax Credit, income limit, single filers: $36,500.

Saver’s Tax Credit, income limit, married couples filing jointly: $73,000.

Health Savings Account Contribution Limit, single coverage: $3,850 (contributor under age 55); $4,850 (contributor 55-plus).

Health Savings Account Contribution Limit, family coverage: $7,750 (contributor under age 55); $8,750 (contributor 55-plus).

High-Deductible Health Plan Minimum Deductible, self-only coverage: $1,500.

High-Deductible Health Plan Minimum Deductible, family coverage: $3,000.

High-Deductible Health Plan Out-of-Pocket Maximum, self-only coverage: $7,500.

High-Deductible Health Plan Out-of-Pocket Maximum, family coverage: $15,000.

2023: Important Tax Dates to Remember

Jan. 1: New IRA, retirement plan, and HSA contribution and income limits go into effect for 2023 tax year, as listed above.

Jan. 17: Estimated tax payments due for fourth quarter of 2022.

April 18:

- Individual tax returns (or extension request forms) due for 2022 tax year.

- Last day to contribute to IRA for 2022 tax year (2022 contribution limits: $6,000 under age 50; $7,000 for age 50 and above).

- Last day to contribute to HSA for 2022 tax year (2022 contribution limits: $3,650 for single coverage, contributor under age 55; $4,650 for single coverage, contributor age 55 and above; $7,300 for family coverage, contributor under age 55; $8,300 for family coverage, contributor age 55 and above).

June 15: Estimated tax payments due for second quarter of 2023.

Sept. 15: Estimated tax payments due for third quarter of 2023.

Oct. 16: Individual tax returns due for taxpayers who received a six-month extension on their 2022 returns.

Dec. 31:

- Retirees age 72 and older must take required minimum distributions from traditional IRAs and 401(k)s; those RMDs are based on their balances at the end of 2022.

- Last date to make contributions to company retirement plans (401(k), 403(b), 457) for 2022 tax year.

This is the 2023 edition of an annual article, and it was previously published on Dec. 15, 2022.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/2OLS3MLLBMTIYCEYJOKJ725MWM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6KYRUHQDUNB6XHNKQ7VMJXDXQY.jpg)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/A6OOX7PBSVEJ5BXDFSPKGLO72M.png)