Are International Stocks Worth the Bother?

While correlations have increased and long-term returns have underwhelmed, recent results look a little brighter.

Vanguard founder Jack Bogle famously argued that international stocks didn’t merit inclusion in investors’ portfolios. He argued that U.S. companies, especially U.S. large caps, derive plenty of their revenue from selling goods and services overseas. So, if non-U.S. economies thrive, investors in U.S. companies should, too.

The past few decades have borne out Bogle’s aversion to non-U.S. equities, as U.S. stocks have handily outperformed non-U.S. stocks. Even investors who buy into the argument that non-U.S. stocks should confer diversification and therefore improve their portfolios’ risk-adjusted performance may be having difficulty keeping the faith.

In our recently published 2023 Diversification Landscape report, we examined the case for international diversification, assessing short- and long-term trends in correlations, returns, and risk. While the correlation between non-U.S. and U.S. stocks has increased over the past several decades, non-U.S. stocks held up slightly better than those in the U.S. in 2022. Moreover, non-U.S. stocks have made a strong case for themselves in certain environments, such as when the dollar has declined relative to other major foreign currencies. As the U.S. market has grown increasingly top-heavy with large technology stocks, non-U.S. indexes’ higher exposure to value sectors should help diversify that bias.

Recent Performance Trends

Even though diversifying into non-U.S. stocks makes intuitive sense and modestly reduced the standard deviation of a U.S.-only portfolio over the past three-, five-, and 10-year periods, doing so has detracted from returns for U.S. equity investors, at least until very recently. In eight of the 10 calendar years from 2013 through 2022, the Morningstar Global Markets ex-US Index lagged the Morningstar US Market Index.

That pattern of underperformance showed signs of reversing in 2022, as non-U.S. stocks held up better than U.S. stocks amid a bear market induced by the Federal Reserve’s aggressive campaign of interest-rate hikes. But that was a modest victory in that most non-U.S. equity indexes endured sharp losses, albeit smaller than what U.S. stocks posted last year. The Morningstar Global Markets ex-US Index lost about 15% last year, compared with a 20% loss for its U.S. counterpart. Emerging-markets stocks lost more than non-U.S. stocks from developed markets last year: The Morningstar Emerging Markets Index shed 18% in 2022 versus a 15% decline for the Morningstar Developed Markets ex-US Index. Although stocks in Latin America and the Middle East performed relatively well thanks to their heavy tilts toward the rallying energy sector, the broad universe of emerging-markets equities sagged in last year’s risk-off environment.

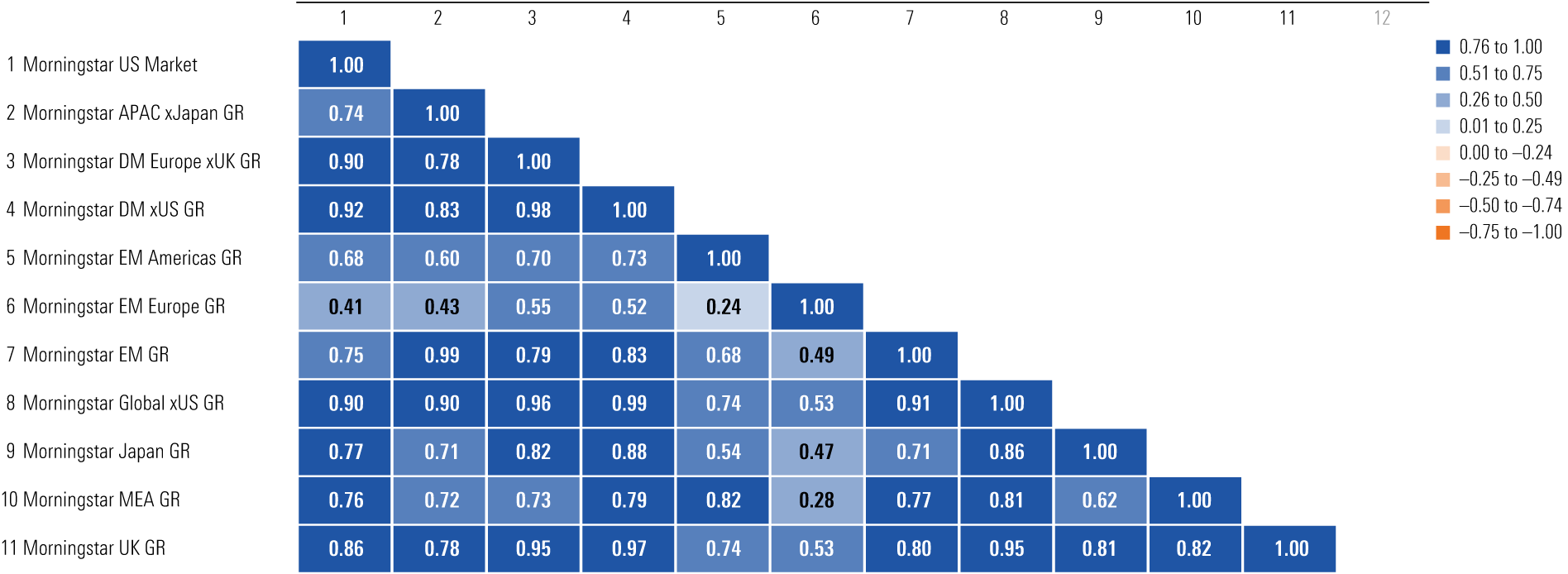

From a diversification perspective, most international-stock benchmarks, especially those in developed markets, have been closely tied to the U.S. market over the past three years, as shown in the exhibit below. Not surprisingly, developed-markets European and U.K. equities have had the tightest correlation with U.S. equities. Meanwhile, emerging-markets stocks have tended to have lower correlations with U.S. stocks.

3-Year Correlation Matrix: International Equity

The small subset of European stocks from markets classified as emerging had the lowest correlation with the U.S. market over the past three years, with correlations declining significantly in 2022. (At the end of 2021, the three-year correlation of the Morningstar Emerging Markets Europe Index with the U.S. market was 0.82; by the end of 2022, it was just 0.41.) That steep drop in correlations owed largely to eastern European equities’ sharp losses following Russia’s invasion of Ukraine in early 2022. The Morningstar Emerging Markets Europe Index lost nearly two thirds of its value last year, a catastrophic loss by any measure and an indication that investors have grave uncertainties about Eastern European markets going forward. Such stocks are just 1.3% of the broader Morningstar Emerging Markets Index, however, and are a negligible slice of the Morningstar Global Markets ex-US Index.

Longer-Term Trends

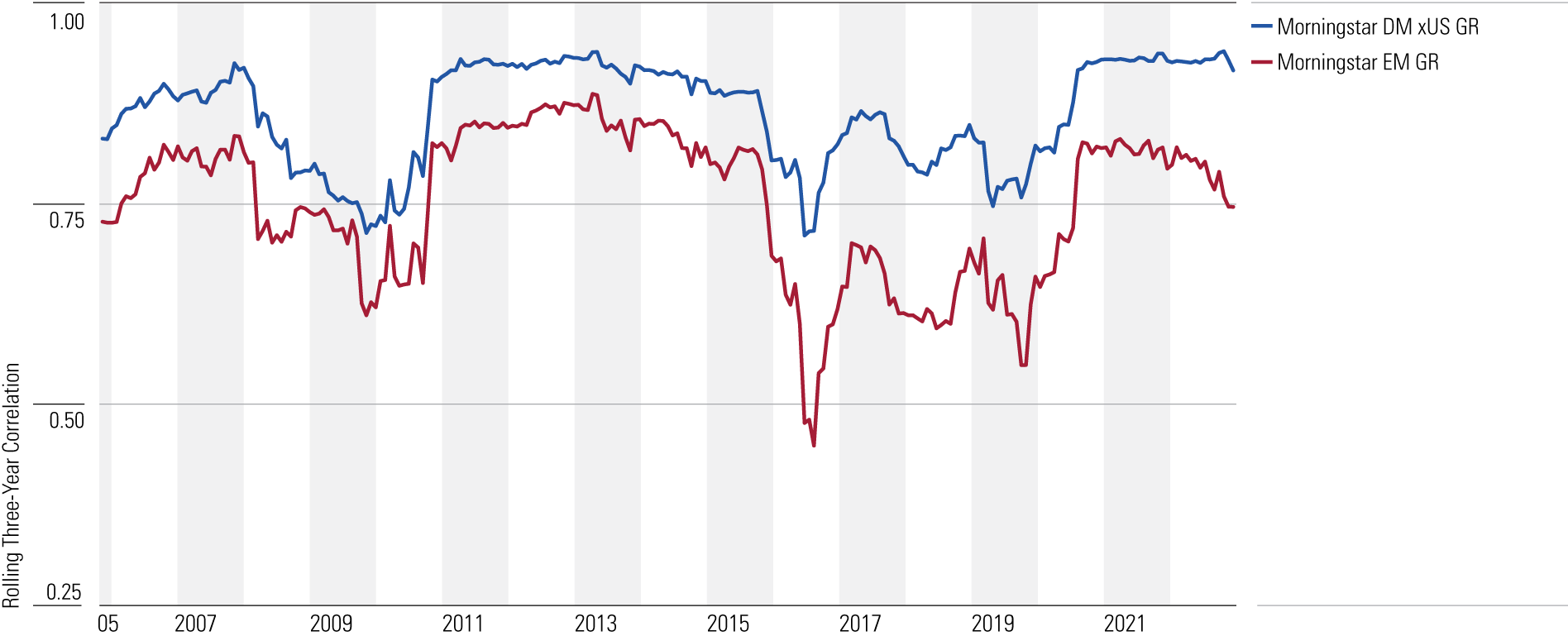

While non-U.S. stocks, especially those from developed markets, have exhibited a high correlation with the U.S. market in recent years, that hasn’t always been the case. As shown in the next exhibit, correlations between the U.S. and international markets have been lower in some previous periods, such as from 2004 through 2008, when the U.S. dollar was generally on the decline. If the greenback goes into another longer-term slump or if the U.S. sinks into recession but other major non-U.S. markets manage to avoid one, it is conceivable that correlations between U.S. and international markets could again drift lower.

Rolling 3-Year Correlations vs. Morningstar US Market Index: International Equity

Longer-term correlations also demonstrate that emerging markets generally have a lower correlation with U.S. stocks than developed markets do. That’s because the types of industries that are especially prominent in emerging markets, particularly energy and basic materials, have declined as a percentage of the U.S. market.

Portfolio Implications

While investors who have diversified internationally haven’t much benefited over the past decade, they have picked up a modest reduction in volatility relative to a U.S.-only portfolio. The 10-year standard deviation of the Morningstar US Market Index is 15.2, whereas the standard deviation of the Morningstar Global Markets Index, which includes both U.S. and non-U.S. names, is 14.4.

Moreover, the U.S. market has become increasingly growth-tilted: 24% of the Morningstar US Market Index lands in the technology sector, for example, whereas just 11% of the Morningstar Global Markets ex-US Index does. The outperformance of technology stocks has redounded to the benefit of U.S.-only investors, as technology names soared for most of the past decade. But in a period in which value-type sectors lead the way, non-U.S. stocks could outperform and help diversify U.S. exposure. Indeed, non-U.S. markets’ slightly higher weighting in energy and lower weighting in technology stocks contributed to smaller losses in 2022 than the U.S. market experienced.

Because emerging markets have generally had a lower correlation with the U.S. equity market than developed, investors seeking diversification may want to make sure their foreign-stock allocation includes at least some exposure to less-developed markets. And while some specific regions have been better portfolio diversifiers than others, most investors will probably want to shy away from investment vehicles that focus solely on a particular geographic region.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)