4 Energy Stocks With Fast-Growing Dividends

A record year of profits means companies such as Devon Energy and EOG Resources are paying buckets of cash to investors.

The gusher of profits that energy companies enjoyed from surging oil and gas prices turned into a bonanza for dividend investors in 2022.

While 2023 isn’t likely to repeat that windfall for investors, dividend growth among energy stocks is still on an upward trend.

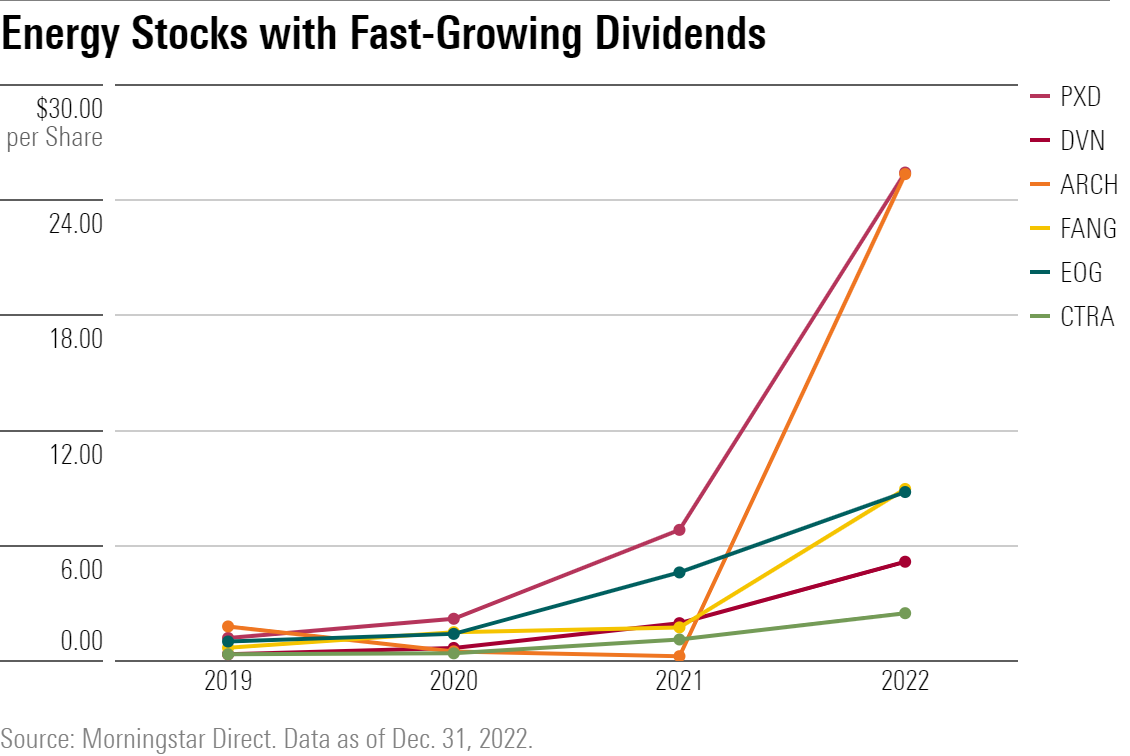

For energy stocks that pay dividends, the average dollar amount paid to investors grew by 390% in 2022, led by oil and gas exploration and production companies such as Diamondback Energy FANG and Pioneer Natural Resources PXD. For the rest of the U.S. market, dividend amounts increased by just 29% on average in 2022.

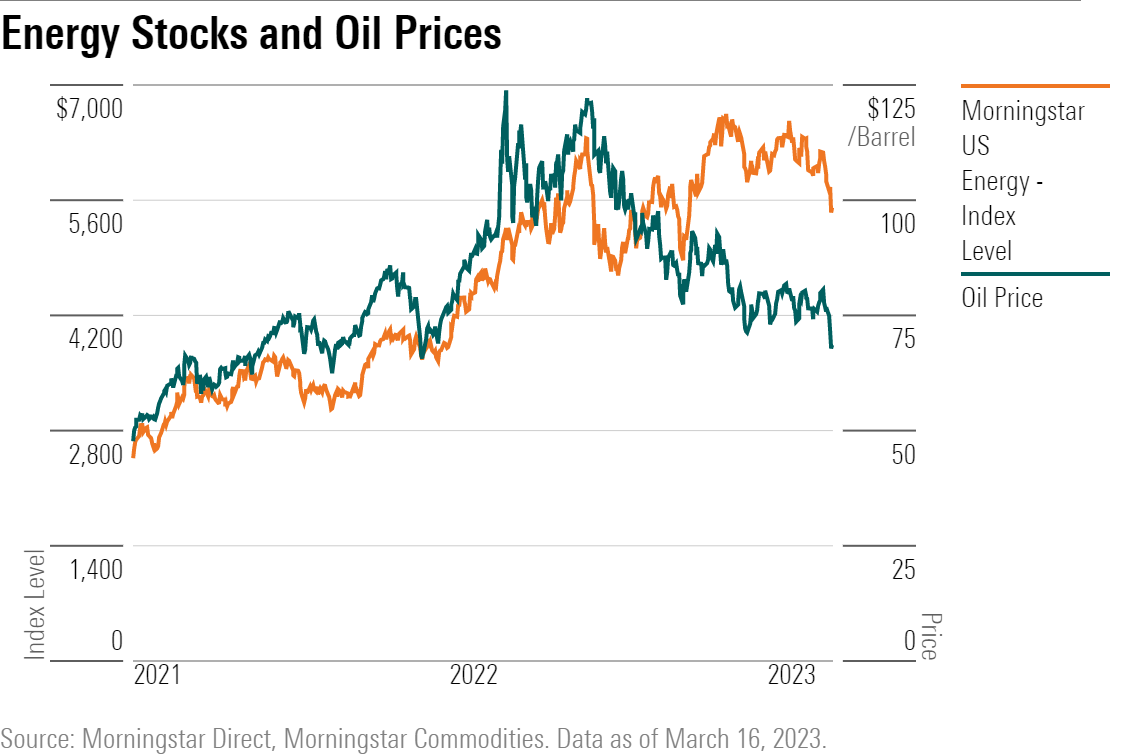

Commodity prices were the key driver of the surge in energy stock dividends: Oil and natural gas price levels both hit multiyear highs in 2022.

In addition, there’s been a longer-standing trend among energy companies—mainly the oil and gas E&P industry—of slowing down their investments into production growth in favor of returning cash to shareholders.

“Energy companies were flush with cash,” says David Meats, director of equity research for energy and utilities at Morningstar. “That gave them the ability to use that cash in several shareholder-friendly initiatives.”

For many energy stocks that pay dividends, this profit boom has translated into a big increase in traditional dividends. There’s also been wider adoption of what are known as variable dividends, a strategy that Morningstar analysts see as often the most attractive option for investors.

What Drove the Outsize Growth of Energy Dividends in 2022?

The exceptional dividend growth for energy companies in 2022 marked a continuation and strengthening of a longer-term trend. Since 2018, energy-stock dividends have grown by 401%. Meanwhile, dividends in the rest of the U.S. market have grown by 86%.

As clean energy investing grows amid increasing concerns about climate change, energy companies face the prospects of a long-term decline in demand for oil and gas. That has translated into a significant change in how companies use the revenue that they generate.

“These companies no longer want to invest as much in their own operations,” Meats says. “They’re adopting corporate strategies of limited production growth.” Returning the extra cash to shareholders is “the best option,” according to Meats.

But surging oil prices were what fueled energy companies’ ability to make these higher dividend payouts over the past year.

“Commodity prices have been the primary driver of the strong growth we saw for energy dividends in 2022,” Meats says. “Because (oil) prices were much stronger in 2022 than they were in 2021, revenues were a lot higher for energy companies,” he adds.

Oil and natural gas prices both hit multiyear highs in 2022: Natural gas prices reached their highest levels since 2008 and crude-oil prices rose to levels not seen in a decade, reaching $106 per barrel in March. That in turn enabled the companies in the Morningstar US Energy Sector Index to generate profits of roughly $254 billion in 2022, up from $77.5 billion in 2021.

At the same time, the Morningstar US Energy Sector Index was far and away the best performer of any U.S. sector index in 2022, gaining 62.5% for its best year in the 24-year history of the index.

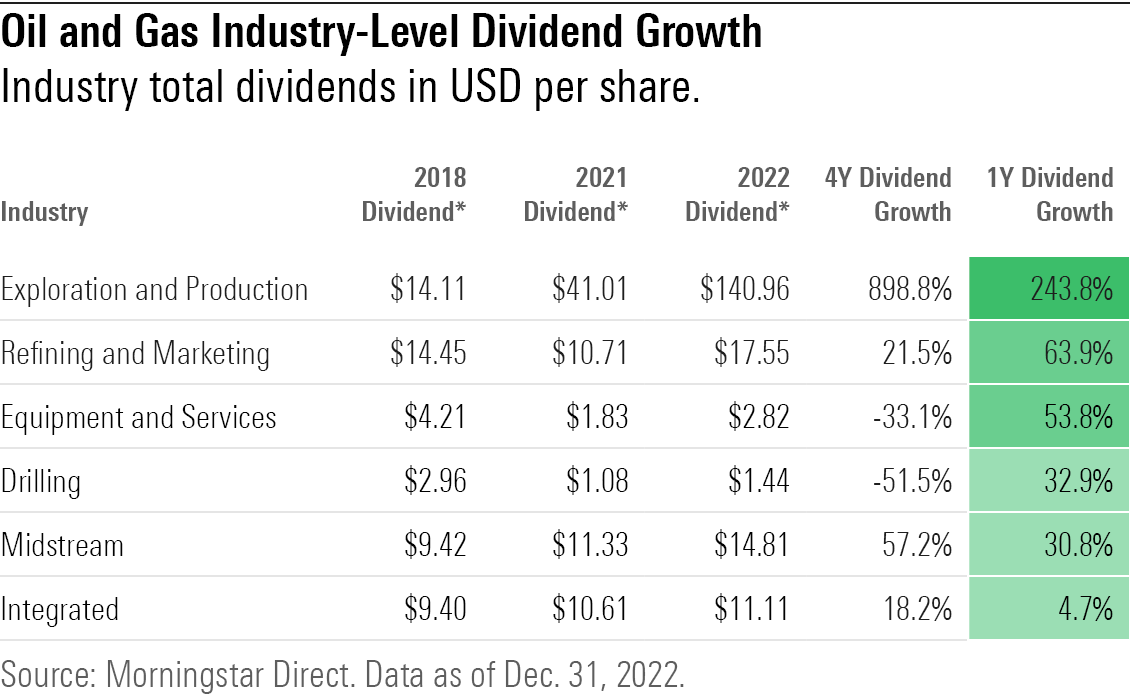

Dividend Growth for Energy Stocks Varies by Industry

At the industry level, the vast majority of the energy sector’s dividends—in terms of both percentage growth and actual dollar amounts—come from oil and gas E&P companies.

This group, which includes companies that primarily focus on finding and extracting new oil reserves, increased its dividend payouts by 243.8% in 2022 alone. Since 2018, dividends in the industry have grown by nearly 900%.

Over the past four years, 18 oil and gas E&P companies (54.5% of all the E&P companies in the Morningstar US Market Index) introduced new dividends. In 2022 alone, five more oil and gas E&P companies introduced new dividends.

Oil and gas refining and marketing companies, which process and sell petroleum products, have also seen substantial growth in dividend payouts, which increased by 63.9% in 2022. Meanwhile, the oil and gas equipment and services industry—a collection of companies that provide tools and solutions for drilling and land surveying—increased its dividends by more than 50% in 2022.

In contrast, outside of the energy sector, dividend-paying companies grew their dividends by 29.3% on average over the course of 2022.

The Most Durable Energy-Dividend Strategies

While the boom was industrywide, there are differences among individual energy companies in terms of how to pass their windfalls on to shareholders. There are traditional fixed dividends, where companies set the payouts in a place and strive to maintain or increase the dividends and avoid lowering them.

Meats says investors and companies benefit from variable dividends. They allow companies to pay out more cash to shareholders when oil prices rise but lower the payout when times get tough, which avoids stressing the companies’ balance sheets.

“Commodity prices are volatile,” Meats says, “variable dividends are a way to signal to the market that in times when there is a lot of excess cash, an energy company will return it to shareholders—and in times when cash is tight, they can be more conservative.” In addition to Pioneer Natural Resources, Devon Energy DVN also offers variable dividends to its shareholders.

In addition, some energy companies are customizing the variable dividend strategy to include stock buybacks when the time is right.

“These management teams are recognizing that there are good times to buy stock and good times to make payments in cash,” Meats says. “They’re always giving back a certain percentage of their free cash flow, but it’s through a hybrid approach: focusing on buybacks when their stocks are cheap and making incremental cash payments at other times.”

Meats says that this combined approach is Morningstar equity analysts’ preferred strategy. Currently, EOG Resources EOG and Diamondback Energy both offer this approach.

The Future for Growing Energy Dividends Is Still Intact

Though 2022 was an outsize year for energy stock dividends, the longer-term trend of growth is likely still intact for the future.

“Energy companies are aiming to return a large portion of their free cash to shareholders, and shareholders are expecting that,” says Meats. “The companies will continue to follow the strategy of growing their dividends, but the dollar amount that actually gets returned over any given year is dependent on the profitability of the companies that year—in large part, that depends on commodity prices.”

In years such as 2022, when commodity prices spiked, shareholder returns will be especially strong. Other years won’t be quite as strong.

“In 2023, you’ll see more moderate returns to shareholders,” Meats says. “And in any case, shareholder returns are still going to be significantly more lucrative than they were in 2016, when the focus for these companies was primarily on drilling new wells.”

4 Energy Stocks With Fast-Growing Dividends

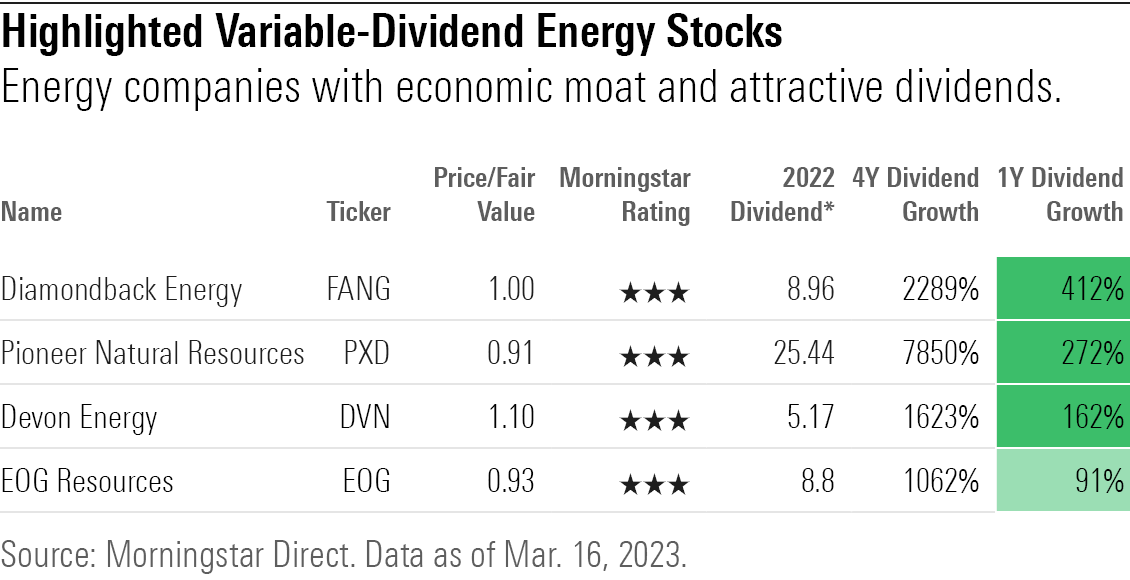

Below are four U.S.-based oil and gas companies within the E&P industry that have been growing their dividends. All four offer one of the variable-dividend strategies that Meats and his team look for. These energy companies have also earned Morningstar Economic Moat Ratings of narrow, meaning they have competitive advantages strong enough to fend off competition and earn strong returns on capital for up to 10 years into the future:

- Diamondback Energy

- Pioneer Natural Resources

- Devon Energy

- EOG Resources

For now, Meats notes, Morningstar equity analysts see these stocks as roughly in line with their fair value estimates—all of them carry a Morningstar rating of 3 stars. But from a dividend standpoint, they’ve got strong practices with variable dividends that they can sustain through all the ups and downs of the market.

Diamondback Energy

- Industry: Oil and Gas Exploration and Production

- Economic Moat: Narrow

- Stock Price: $125.53

- Morningstar Fair Value Estimate: $126

“Diamondback Energy was a modest-size oil and gas producer when it went public in 2012, but it has rapidly become one of the largest Permian-focused oil firms through a combination of organic growth and corporate acquisitions, most recently Firebird Energy and Lario Permian in 2022. The firm consistently ranks among the lowest-cost independent producers in the entire industry, supporting a maintainable margin advantage.”

“Because of its enviable Permian Basin acreage, Diamondback Energy is the lowest-cost producer in the upstream oil and gas segment. As such, the company is better positioned to cope with weak oil prices than most peers, and at our midcycle forecast—currently $55/barrel (West Texas Intermediate)—it can really thrive. Accordingly, we award a narrow moat rating.”— David Meats

Pioneer Natural Resources

- Industry: Oil and Gas Exploration and Production

- Economic Moat: Narrow

- Stock Price: $186.49

- Morningstar Fair Value Estimate: $205

“Pioneer Natural Resources is one of the largest Permian Basin oil and gas producers overall, and is the largest pure play. It has about 800,000 net acres in the play, all of which is located on the Midland Basin side where it believes it can get the best returns. The firm acquired the bulk of its acreage well before the shale revolution began, with an average acquisition cost of around $500 per acre. That’s a fraction of what most of its peers shelled out during the land grab at the beginning of the Permian boom, giving the firm a unique advantage. And the vast majority of this acreage is located in the core of the play, where well performance is typically strongest. That gives Pioneer an extensive runway of low-cost drilling opportunities.”

“We believe Pioneer has the ability to earn maintainable excess returns on invested capital, justifying a narrow moat rating. The company operates exclusively in the Permian Basin, which is the cheapest source of crude oil in the U.S.—sitting below other shale plays, deep-water projects, and all other unconventional sources on the global cost curve. Pioneer is ideally located within the play as well. That’s important because the precise surface location of a horizontal shale well plays a huge part in determining its eventual productivity and also influences the oil content of its production stream. By focusing on areas that typically yield very impressive initial flow rates, Pioneer’s fixed costs, such as drilling and completions, are spread more thinly, delivering more bang for the buck. The firm’s ideally located acreage also supports above-average unit revenue, as oil cuts are generally strong.”— D.M.

Devon Energy

- Industry: Oil and Gas Exploration and Production

- Economic Moat: Narrow

- Stock Price: $46.27

- Morningstar Fair Value Estimate: $42

“Devon Energy is an oil and gas producer based in Oklahoma. It has assets in several shale basins across the United States, including the Delaware Basin, Eagle Ford Shale, STACK, and Powder River Basin. Management has reshuffled the portfolio in the last few years, divesting its Canadian oil sands business and exiting the Barnett Shale natural gas play. In January 2021, it combined with another Oklahoma-based shale firm, WPX Energy, in a ‘merger of equals’ that significantly expanded Devon’s Delaware Basin exposure and added a small position in the core of the Bakken Shale fairway in North Dakota. The merger brought economies of scale and more efficient field operations, and enhanced the competitiveness of the combined firm.”

“Devon has an inherent cost advantage baked into its asset portfolio (Rystad Energy ranks Devon first among U.S. E&Ps on breakeven costs associated with undeveloped reserves, ahead of several narrow-moat firms such as Diamondback Energy and EOG Resources). This enables the company to reliably deliver excess returns on invested capital, which are a hallmark of moaty companies in our framework. We therefore assign a narrow moat rating.”— D.M.

EOG Resources

- Industry: Oil and Gas Exploration and Production

- Economic Moat: Narrow

- Stock Price: $104.48

- Morningstar Fair Value Estimate: $112

“EOG Resources is one of the largest independent oil producers. Most of its production comes from shale fields in the U.S., with a small contribution from Trinidad. The firm differentiates itself by looking for prospective areas before most peers catch on, enabling it to secure leasehold at attractive rates (rather than overpaying for land after the market overheats). It has only one large-scale M&A deal under its belt, related to its 2016 entry to the Permian Basin. Nevertheless, the firm is also active in most other name-brand shale plays, including the Bakken and Eagle Ford. Additionally, the focus now includes the Powder River Basin (Wyoming) and a new natural gas play in southern Texas that the firm has christened ‘Dorado.’”

“Until recently, very few shale producers were paying attention to shareholder returns, but EOG was one of them. The firm actually delivered excess returns on invested capital for five of the six years of 2009-14, before the downturn in global crude prices began. That pushed returns back in negative territory for several years. But a relentless focus on cost-cutting, productivity, and efficiency eventually paid off, enabling EOG to start earning its cost of capital again and qualifying the firm for a narrow moat rating.”— D.M.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/UYSRGR6ZLJFWXDECADZPSR7BJU.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MLKHO4HEDJETLPBTREPIAMGQBE.png)